You earn a decent income. Yet somehow, by the end of the month, you are left wondering where all your money went. Sound familiar? If so, you are not alone. Millions of people around the world struggle with managing their finances — not because they do not earn enough, but because they have never had a clear, simple framework to follow. Therefore, the 50/30/20 budget rule might be exactly what you need. Moreover, it is one of the most widely recommended personal finance strategies precisely because it is so simple that virtually anyone can follow it — starting today.

In this complete guide, we will break down exactly what the 50/30/20 budget rule is, how it works in practice, who it is best suited for, and how you can immediately start applying it to your own financial life.

What Is the 50/30/20 Budget Rule?

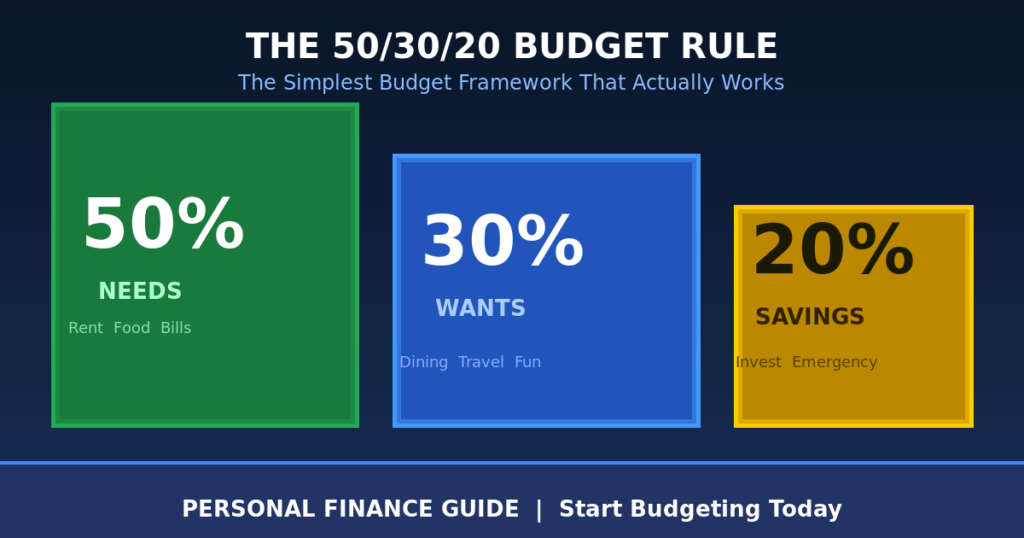

The 50/30/20 rule is a straightforward budgeting framework that divides your after-tax income into three categories using fixed percentage allocations. It was popularized by US Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their book All Your Worth: The Ultimate Lifetime Money Plan. However, the underlying principle has been a cornerstone of sound financial planning for decades.

Furthermore, the beauty of this rule lies in its simplicity. Instead of tracking every single expense in exhausting detail, you simply ensure that your spending falls within three broad buckets. As a result, budgeting becomes something you can actually maintain long-term rather than a system you abandon after two weeks.

Breaking Down the Three Categories

50% — Needs: The Non-Negotiables

The first and largest portion of your budget — 50% of your after-tax income — is allocated to needs. These are essential expenses that you genuinely cannot live without. Moreover, needs are the financial obligations that would cause serious problems if left unpaid.

Examples of needs include:

- Housing: Rent or mortgage payments, property taxes, and essential home maintenance.

- Utilities: Electricity, water, gas, and basic internet connection.

- Groceries: Basic food and household supplies — not dining out or premium items.

- Transportation: Car payments, fuel, public transport, or essential vehicle maintenance.

- Insurance: Health, auto, and home or renters insurance premiums.

- Minimum Debt Payments: The minimum required payments on loans or credit cards.

However, it is important to be honest with yourself about what truly qualifies as a need versus a want. A basic smartphone plan is a need. The latest iPhone on an expensive contract is likely a want. Therefore, this distinction is crucial for the rule to work effectively.

30% — Wants: The Quality-of-Life Expenses

The second category — 30% of your after-tax income — covers wants. These are the expenses that enhance your life and bring enjoyment, but that you could technically live without. Furthermore, this is the category that most people either overspend dramatically or feel guilty about entirely — and the 50/30/20 rule elegantly solves both problems by giving wants a legitimate, budgeted place in your finances.

Examples of wants include:

- Dining Out and Takeaways: Restaurants, coffee shops, food delivery apps.

- Entertainment: Streaming subscriptions, cinema, concerts, sports events.

- Shopping: Clothing beyond basics, gadgets, home decor, and lifestyle purchases.

- Travel and Holidays: Vacations, weekend getaways, and leisure travel.

- Gym and Hobbies: Fitness memberships, sports, creative pursuits, and personal interests.

- Personal Care Upgrades: Premium grooming, beauty treatments, and wellness services.

Importantly, the 30% wants allocation is not something to feel guilty about. In addition, having a guilt-free spending category actually makes budgets more sustainable, because people are far more likely to stick to a system that allows them to enjoy their money rather than one that feels like punishment.

20% — Savings and Debt Repayment: Building Your Future

The final and arguably most important category is the 20% allocated to savings and additional debt repayment. Moreover, this is the portion of your income that builds financial security, creates opportunity, and ultimately gives you the freedom to live life on your own terms.

This 20% should ideally be split across:

- Emergency Fund: Building 3-6 months of living expenses as a financial safety net. This is the first priority for anyone starting out.

- Retirement Savings: Contributions to pension plans, 401(k), or equivalent retirement accounts.

- Investments: Stocks, index funds, real estate, or other wealth-building vehicles.

- Additional Debt Repayment: Paying above the minimum on high-interest debt like credit cards. Consequently, this reduces the total interest paid and accelerates financial freedom.

- Specific Savings Goals: A house deposit, a new car, education, or any other major planned expense.

Real-World Example: How the 50/30/20 Rule Works in Practice

Let us apply the 50/30/20 rule to a concrete example. Therefore, consider someone with a monthly after-tax income of ,000:

| Category | Percentage | Monthly Amount | Examples |

| Needs | 50% | ,500 | Rent, utilities, groceries, transport |

| Wants | 30% | 00 | Dining, streaming, shopping, travel |

| Savings/Debt | 20% | 00 | Emergency fund, investments, extra debt payments |

Furthermore, here is the same rule applied to a higher income of ,000 per month:

| Category | Percentage | Monthly Amount | Examples |

| Needs | 50% | ,000 | Mortgage, car, insurance, food |

| Wants | 30% | ,800 | Holidays, restaurants, hobbies, subscriptions |

| Savings/Debt | 20% | ,200 | Retirement fund, investments, debt payoff |

Who Is the 50/30/20 Rule Best Suited For?

One of the greatest strengths of the 50/30/20 rule is its versatility. However, it is particularly well-suited for certain groups of people.

- Budgeting Beginners: If you have never followed a budget before, the simplicity of three categories makes this the ideal starting point. Moreover, it requires no spreadsheets or complex tracking apps to implement.

- Middle-Income Earners: The rule works best for people whose income comfortably covers their needs. As a result, they have genuine flexibility in the wants and savings categories.

- People Who Have Tried and Failed at Budgeting: Detailed budgets that track every category often fail because they are too restrictive and time-consuming. Therefore, the 50/30/20 rule offers a more forgiving and sustainable alternative.

- Young Professionals Starting Out: The 20% savings habit, when started early, has an enormous compounding effect over time. Furthermore, building this discipline in your twenties creates financial security that compounds for decades.

Common Challenges and How to Overcome Them

Challenge 1: Needs Exceed 50%

This is the most common difficulty people encounter, particularly in high cost-of-living cities where housing alone can consume more than 50% of income. Therefore, if your needs genuinely exceed 50%, you have several options: look for ways to reduce fixed costs (a cheaper apartment, refinancing a loan), increase your income, or temporarily adjust the percentages while working toward a better balance. As a result, the rule becomes a target rather than a rigid constraint.

Challenge 2: Distinguishing Needs From Wants

Many people initially struggle to categorize expenses accurately. Moreover, lifestyle inflation — the tendency to treat luxury items as necessities over time — can blur these lines significantly. Therefore, a useful test is to ask: would my health, safety, or employment be seriously at risk without this expense? If the answer is no, it is likely a want rather than a need.

Challenge 3: Staying Consistent Month to Month

Some months bring irregular expenses — car repairs, medical bills, or annual subscriptions. Furthermore, these can throw off the percentages temporarily. Consequently, the solution is to either build a sinking fund within your savings category for predictable irregular expenses, or to view the 50/30/20 rule as an average across three to six months rather than a perfect monthly target.

How to Start Using the 50/30/20 Rule Today

Getting started is simpler than most people expect. Therefore, here is a clear step-by-step process:

- Step 1 — Calculate Your After-Tax Income: Include your salary after all deductions, plus any additional income sources like freelance work or rental income.

- Step 2 — List All Your Current Expenses: Go through your last two to three months of bank and credit card statements. Moreover, categorize each expense as a need, want, or savings contribution.

- Step 3 — Calculate Your Current Percentages: Add up your totals in each category and divide by your monthly income. As a result, you will see exactly where you stand versus the 50/30/20 targets.

- Step 4 — Identify the Gaps: Most people discover they are overspending on wants and underspending on savings. Furthermore, simply identifying this gap is often the most motivating realization.

- Step 5 — Automate Your Savings: Set up an automatic transfer of 20% of your income to a separate savings or investment account on payday. Consequently, the money is never available to spend impulsively.

- Step 6 — Review Monthly: Spend 15 minutes at the end of each month reviewing your spending. Moreover, adjust as needed without guilt — the goal is progress, not perfection.

Conclusion

The 50/30/20 budget rule is not a magic solution that eliminates financial stress overnight. However, it is one of the most practical, sustainable, and psychologically sound approaches to personal finance ever developed. Therefore, if you have struggled with budgeting before, this framework gives you a fresh start with a system that is actually designed to succeed.

Moreover, the most important thing is simply to begin. Even imperfect implementation of the 50/30/20 rule will produce meaningful improvement over having no budget at all. As a result, one month from now, you could have a clearer picture of your finances, a growing emergency fund, and — perhaps most importantly — the confidence that comes from knowing your money is working for you rather than mysteriously disappearing.

Frequently Asked Questions (FAQs)

Q1: Should I apply the 50/30/20 rule to my gross or after-tax income?

Always use your after-tax income — the actual amount that lands in your bank account after all taxes and mandatory deductions. Furthermore, using gross income will overestimate your available budget and cause the percentages to be misleading.

Q2: What if I have significant debt? Should savings still be 20%?

If you carry high-interest debt, it is often wise to prioritize aggressive debt repayment within the 20% category. Moreover, paying off a credit card at 20% interest is effectively the same as earning a guaranteed 20% return on investment — which is exceptional. Therefore, direct most of your 20% toward debt until high-interest balances are cleared.

Q3: Can I adjust the percentages?

Absolutely. The 50/30/20 rule is a guideline, not a law. Furthermore, your circumstances may justify a 60/20/20 split if you live in an expensive city, or a 40/20/40 split if you are aggressively saving for retirement. As a result, the key principle is intentional allocation — the specific percentages can flex to suit your reality.

Q4: Is the 50/30/20 rule suitable for low-income earners?

It can be challenging for very low-income earners whose necessities genuinely consume more than 50% of their income. However, the rule still provides a useful framework and aspirational target. Moreover, even small, consistent contributions to savings — well under 20% — build meaningful financial resilience over time.

Q5: What is the best app to track the 50/30/20 rule?

Several budgeting apps support the 50/30/20 framework directly, including YNAB (You Need A Budget), Mint, and PocketGuard. Furthermore, a simple spreadsheet works just as effectively for people who prefer a manual approach. Consequently, the best tool is whichever one you will actually use consistently.